Bản tin chiến lược đầu tư tuần 30.06 – 04.07.2025

Tóm tắt báo cáo

- Ngày 24.06, NHNN bất ngờ phát hành tín phiếu trở lại sau 4 tháng tạm dừng. Động thái trên của NHNN diễn ra trong bối cảnh tính từ đầu năm đến nay, tỷ giá USD/VND đã tăng gần 3% bất chấp chỉ số DXY – thước đo sức mạnh của đồng bạc xanh trên thị trường quốc tế – giảm khoảng 9%.

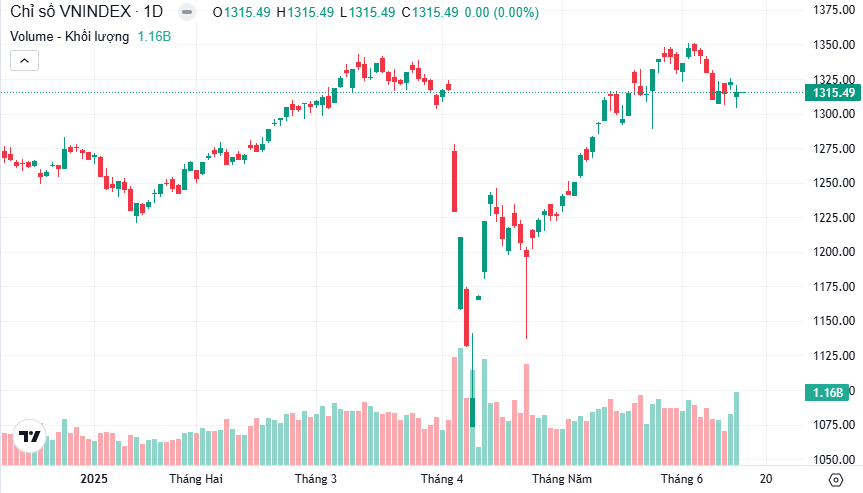

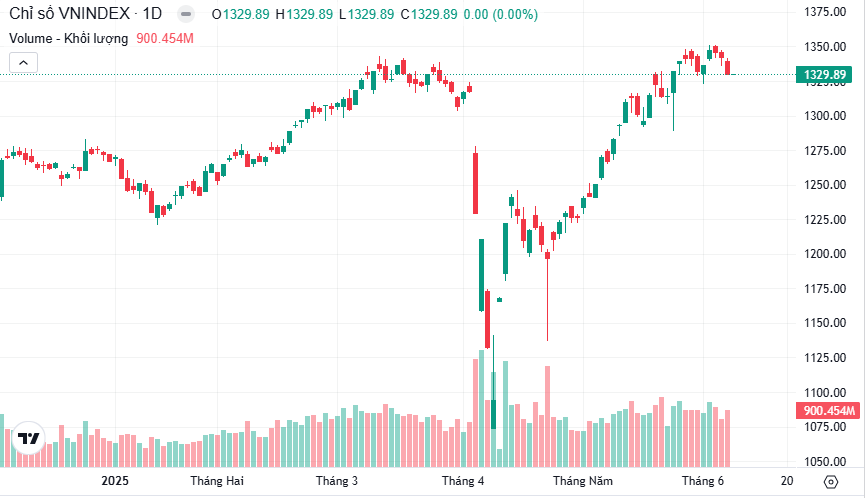

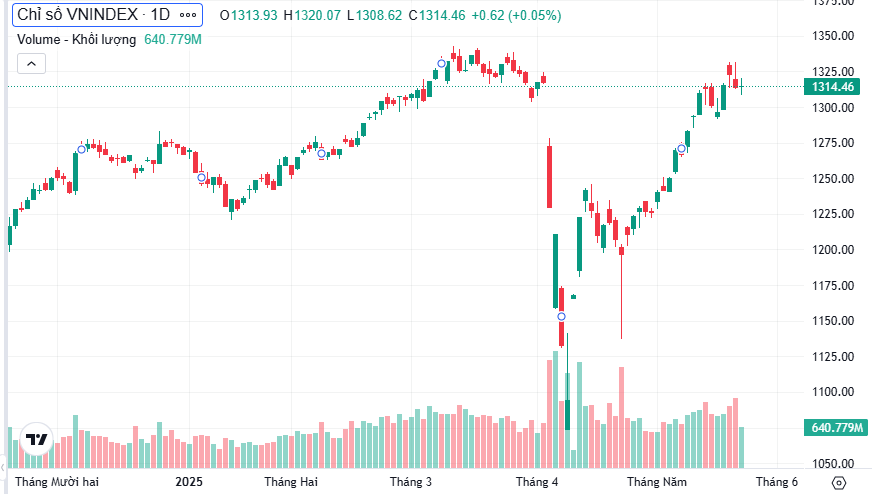

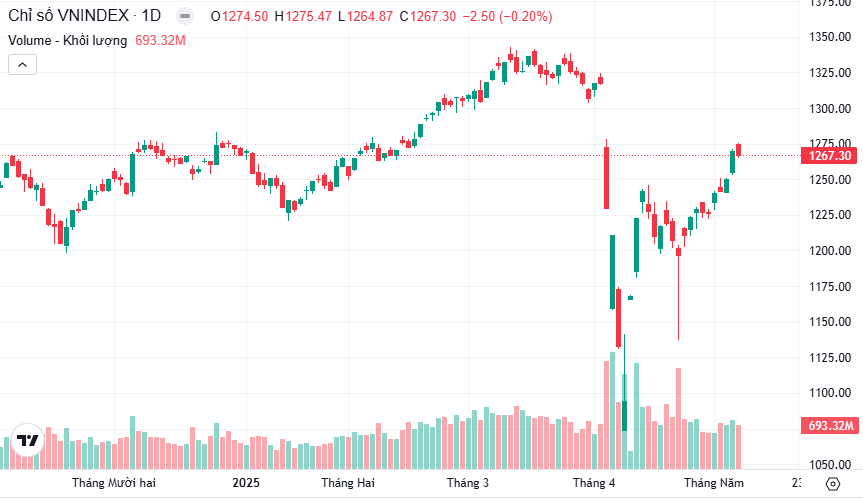

- Trong tuần qua, VN-Index ghi nhận tăng 1.61% lên mốc 1,371.44 điểm, với dòng tiền chảy vào thị trường ghi nhận tín hiệu trái chiều, với khối lượng và giá trị giao dịch trung bình mỗi phiên trong tuần qua, đạt giá trị lần lượt là 832 triệu cổ phiếu và 21,422 tỷ đồng. Dòng tiền ghi nhận chảy vào mạnh nhất tại nhóm bất động sản (6.79%) và thực phẩm, đồ uống (4.64%).

- Hiện tại, chỉ số VN-Index đang ghi nhận xu hướng đi ngang trở lại trên khung tuần với vùng hỗ trợ ngắn hạn gần nhất nằm tại mốc tâm lý 1,280 – 1,300 điểm. Dự báo trong tuần 30.06 – 04.07.2025, dự kiến chỉ số VN-Index sẽ tiếp tục ghi nhận diễn biến rung lắc mạnh và dao động trong vùng 1,360 – 1,385 điểm trong bối cảnh thị trường đang bước vào vùng trũng thông tin; áp lực chốt lãi ngắn hạn gia tăng; kết quả đàm phán chính thức giữa Việt Nam và Mỹ về thuế quan đối quan đối ứng vẫn khó đoán định; NHNN phát đi tín hiệu can thiệp tỷ giá thông qua phát hành tín phiếu, ảnh hưởng đến tâm lý nhà đầu tư; thời hạn hoãn thuế quan đối ứng đang đến gần nhưng vẫn chưa có nhiều thỏa thuận giữa Mỹ và các đối tác được ký kết

- Nhà đầu tư được khuyến nghị hạ tỷ trọng danh mục quanh ngưỡng 30% – 40%, đồng thời chỉ tập trung nắm giữ các cổ phiếu có câu chuyện tăng trưởng riêng và không bị ảnh hưởng bởi chính sách thuế quan đối ứng của Mỹ.

- Một số nhóm cổ phiếu đáng quan tâm trong giai đoạn hiện nay bao gồm:

- Nhóm cổ phiếu trading ngắn hạn

- Nhóm ngân hàng: CTG, BID

- Nhóm bán lẻ: MWG

- Nhóm bất động sản khu công nghiệp: KBC

- Nhóm cổ phiếu nắm giữ trung hạn

- Nhóm ngân hàng: TCB;

- Nhóm cổ phiếu nắm giữ dài hạn

- Nhóm ngân hàng: VPB

- Thép: HPG

- Nhóm cổ phiếu trading ngắn hạn